This initiative is based on an MOU to establish the Strategic Talent Center (“STC”) as a platform that engages with the private sector. STC is the mechanism that assesses foreign experts in digital technology and sciences who wish to live and work in Thailand. The applicant must be employed by a Thai employer such as a limited liability company, but there is no restriction in regards to registered capital or numbers of employees. The company should apply for the qualification / expertise recognition through STC, who will then refer the application to the relevant officials for final evaluation. Once the application is accepted, they will then be granted an annual visa and work permits.

Experts who have been accepted by STC will receive visa and work permit benefits, even if they do not work in a BOI-promoted company. Moreover, STC-recognized foreign experts can access services at the One Stop Service Center for Annual Visa and Work Permit, usually reserved for BOI-promoted companies.

Additionally, the government accepts the principle of four-year visa-free grants and free work permits under a new scheme labelled the “Smart Visa”. The visa is targeted to industry experts and foreign technology investors. Currently, foreigners in Thailand must report to authorities every 90 days. Under the “Smart Visa” scheme, holders will be required to report to the immigration bureau only once a year. This visa will be extendible to family members.

The scheme is still in a testing stage and is undergoing an impact study. The government plans to issue and enforce the “Smart Visa” by next year.

The plan was first proposed in March 2016, in order to attract investment and talented foreign workers. The government has stated that the new visa is intended to facilitate knowledge transfer to boost business growth in Thailand, and lead to long-term economic development. Under the current structure, foreign investors and experts are offered visa grants up to two years.

Applications for the new “Smart Visa” may be accepted as soon as January 2018. To keep up to date on developments and for more information about setting up a business in Thailand, please contact [email protected]

Comments Off on 10-year Thailand Visas now Available

The 10-year visa for foreign retirees is now available. This comes after last year’s cabinet resolution, which agreed to permit this type of visa. The official announcement of the Ministry of Interior dated 26 May 2017 came into full force on 26 July 2017. Applications for 10-year visas are already being accepted. Foreigners can apply at their provincial immigration offices.

Importantly, foreign retirees must meet the requirements. Of note is the required deposit amount of 3 million THB and to hold a passport from one of 14 countries: Australia, Canada, Denmark, Finland, France, Germany, Italy, Japan, Netherlands, Norway, Sweden, Switzerland, the United Kingdom or the United States.

Feel free to contact us if you have any questions: [email protected]

Comments Off on “Thailand 4.0” – A New Era for Thailand’s Economy

Before Thailand jumped into the 4.0 era, there was Thailand 1.0 which was based on the agriculture sector, Thailand 2.0 focused on light industry and then came the heavy industry of Thailand 3.0 which caught the nation in a medium income trap, with growing income inequality and imbalanced development. Now, the government is planning a 20-year National Strategic Plan to strengthen the local economy through “Sufficiency Economy” and to connect better with world markets.

The government intends to transform three main areas:

1. From producing “consumer goods” to creating “innovative” value-added products

2. From an emphasis on physical capital to shift the focus on human capital, technology, innovation, and creativity

3. From a production based to service-based economy

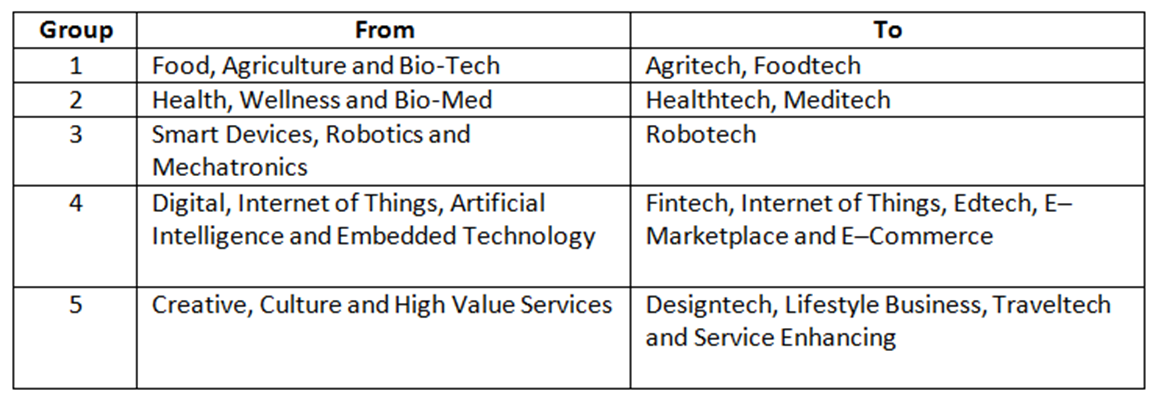

Under the “Thailand 4.0” model, the nation’s economy will be innovation driven by upgrading technology, improving creativity, innovation, and research and development capacity of five target industries to create “New Startups” as demonstrated in the table below:

The Thai government’s vision represents a starting point to transform the country towards stability, prosperity, and sustainability, which aims to drive Thailand to a more prosperous future.

Feel free to contact us if you have any questions: [email protected]

Comments Off on Thailand Ranks 19th in global FDI Confidence Index on Long-term Economic Potential

According to the Thai Board of Investment, Thailand’s ranking in the A.T. Kearney Foreign Direct Investment (FDI) Confidence Index 2017 has been improved to 19th ranking thanks to the country’s long-term economic potential and committed support from the Thai government, including attractive investment promotion incentives and tools. China ranked 3rd in the index while Japan ranked 6th and Singapore ranked 10th.

The Index indicated that investor confidence in Thailand is growing as 21% as the respondents in this year’s survey said they were optimistic about Thailand’s economic outlook over the next three years.

Comments Off on Obtaining a Work Permit in Thailand

Work Permit Requirements

As in any other country in the world, foreigners require a governmental permission prior to working in Thailand. In this article, we will explain the administrative process related to the application for a work permit. Individuals applying for Thai work permits must qualify under the Thai law. The applicant must have the knowledge or skills to perform the work as stated in the description of the position provided in the application for the work permit. Thai law also requires that the foreign national is not insane or mentally sick, nor sick of leprosy, tuberculosis, drug addiction, alcoholism and elephantiasis, and not having been imprisoned for violations of the immigration law or the foreign employment law in the year before applying for a work permit.

The “Land of Smiles” is an attractive destination for both tourists seeking fun and professionals seeking opportunities. However, the Kingdom of Thailand has many regulations concerning travel and residence in the country. Foreign nationals must obtain visas if they wish to enter the Kingdom. Thailand is also a party to many bi-lateral agreements which allow citizens of certain foreign countries to stay for short periods without having to obtain a visa. Thailand also has provisions to allow foreign nationals to apply for work permits to work in the Kingdom.

1. Entry Visas

The laws and regulations regarding visa and work permit in Thailand are extensive, and the Immigration Bureau frequently revises its regulations to adjust to new circumstances and policies. It should further be noted that the various Thai embassies and consulates have specific policies which may vary.

Foreign nationals of the country that made an agreement with the Thai government according to Interior Ministerial Regulation shall be permitted to stay in Thailand according to the period which is mutually agreed between Thailand and the respective other country. Foreign nationals from 42 countries and Hong Kong SAR will be able to enter into the Kingdom of Thailand without a visa and stay in Thailand for 30 days per each visit (“Visa Exemption“). However, the total duration of stay shall not exceed 90 days within a six month period, counting from the date of the first entry.

Tourists who wish to enter the Kingdom must apply for a Tourist Visa with the Royal Thai Embassy or Consulate in their country. A tourist visa is for a maximum duration of 60 days (depending on nationality), for the purpose of tourism only and may be extended for another 30 days (depending on nationality).

Foreigners who wish to work or conduct business in Thailand should apply for a non-immigrant-B-visa. This visa may be issued by an embassy or consulate abroad. There are different types for this kind of visa, namely a single entry visa with permission to stay for 30 days and a multiple re-entry visa which is issued for one year but permission to stay for only 90 days and the requirement to do so-called “visa runs”. The non-B visa can be issued for foreigners doing business in Thailand or for employment.

There are various other types of visa, permitting to stay in Thailand on the basis of marriage, retirement, diplomatic status, etc.

Obtaining a One Year Visa (Visa Extension)

The consideration of permission for a foreign national to temporarily stay in Thailand for one year without the need of visa-runs (‘Visa Extension”, issued by the Immigration Office in Thailand) must follow the following rules and documents listed below:

1. That foreign national must have a Non-Immigrant visa, and

2. the foreign national must have an income in the amount of 50,000 THB (for citizens of Europe, Australia) or in the amount of 60,000 THB (for Japan, Canada and United States of America) or in the amount of 45,000 THB (for Korea, Singapore, Taiwan, Hong Kong SAR and Malaysia) or in the amount of 35,000 THB (for Asia and South America).

3. The employer must have a registered capital of not less than Two Million THB, and

4. The employer must have submitted a balance sheet of the last financial year which has been audited by a certified public accountant in order to show a good financial standing. The total of Shareholders’ Equity in the balance sheet will not be less than One Million Thai Baht, and

5. The employer must have submitted a profit and loss statement (Statement of Income) that has been audited by a certified public accountant (the year end date must be the same date on the balance sheet and the total revenue in the said Statement of Income must not be less than the total money that the business is required to pay for salary for every foreign national), and

6. The employer is required to hire a foreign national, and

7. The employer must have a ratio of employment of one foreign national per four permanent Thai staff.

Under current Immigration Regulations, if a foreign national stays in Thailand for a period longer than 90 days, he/she must notify the Immigration Division (“90 days reporting”). This regulation applies even after the foreigner has obtained a one-year visa. This 90-day period is calculated from the date the foreigner last checked through Immigration.

Please feel free to contact us if you have any inquiries regarding the above: [email protected]

Our next blog article will explain the process of applying for work permits in Thailand, sign up to our newsletter and we’ll send you articles like this every month.

Many foreigners aspire the purchase of a condominium unit in Thailand, for either residential or investment purposes.

1. Foreign Ownership

Foreigners are allowed to buy and own a condominium unit in Thailand. However, only condominiums registered under pertinent laws and licensed with the Thai Land Department offer full individual ownership (with a government-issued unit ownership title deed) and are regulated by the Thailand Condominium Act.

At least 51% of the area of the condominium building must always be Thai owned. The foreign-owned units are often referred to as “foreign freehold” units or units held under the “foreign quota”. If the foreign freehold ownership in a condominium has reached the limit of 49%, the remaining units may be leased to foreigners under a 30-year lease agreement. This is often referred to as “leasehold unit”.

There are no restrictions with regards to nationality, and any foreigner who can enter Thailand with a valid visa can buy and own a condominium unit within the foreign ownership quota of the condominium.

2. Transfer of Foreign Currency is Required

The purchase price for the condominium must be transferred into Thailand in foreign currency and converted into Thai Baht by a licensed financial institution within Thailand.

For a foreigner buying a condominium a proof of fund or the so-called “FET-Form” form (Foreign Exchange Transaction Form) or the bank certificate, with his name either as the receiver or sender of the foreign currency, is part of the required documents for registration of foreign ownership at the Land Department.

Option 2:Paying in Thai Baht from a Non-Resident Account

It is possible to pay in Thai Baht for a condominium if you have the funds in a non-resident account opened with the bank in Thailand. With this method, you must have a certificate from your bank that certifies that you withdraw Thai Baht from your non-resident account in the amount of not less than the price of a condominium unit which you are going to buy. In that certificate, it should state that the money you withdraw is for buying a condominium.

If you are married, you need to present a Marriage certificate during the registration for official records.

3. Ownership Transfer – Fees and Taxes

In general, the current fee and taxes applicable to and payable upon the registration of ownership of a condominium unit are as follows:

a. Transfer fee:

2% of the value of the condo unit (as appraised by the land office).

b. Income Tax:

Income tax (withholding tax) at the rate of 1% of the land office appraised or the actual transaction value of the condominium unit (whichever is higher) applies if the seller is a juristic person. This is a withholding tax, and it is credited to (i.e. deducted from) the company’s income tax payable for that year.

An incremental personal income tax with a sliding scale from 0% – 35% based on the value of the property (as appraised by the land office) applies if the seller is an individual and gain a profit, the seller shall be obligated to be liable for tax filing and payable to the Revenue Department.

c. Stamp Duty or Specific Business Tax:

Either Stamp Duty at the rate of 0.5% of the appraised or the actual transaction value of the property (whichever is higher) applies or Specific Business Tax at the rate of 3.3% of the appraised or the actual transaction value of the property (whichever is higher). In general, the Stamp Duty will apply if the land has not been transferred within the last five years. Otherwise the Specific Business Tax will always apply.

4. Taxation of Income Derived from the Unit

Rental income, as well as proceeds of a resale, are subject to income tax. Profits derived from property in Thailand are taxable in Thailand. According to Double Taxation Agreements, they are taxable only in Thailand.

Generally, the tax rates are as follows:

a. Tax rate for corporate taxpayer: 20% (current rate, reduced for small and medium-sized companies)

b. Tax rate for individual taxpayer: 0-35% (sliding scale, please see above regarding the discharge from tax liability in case of a resale)

Rental income must be declared in an annual tax return. For a corporate taxpayer, also the proceeds from a sale must be declared.

Furthermore, Land and House Tax (often referred to as “Structure Usage Tax”) is imposed on the owners of a Condominium unit, except for the first residential place. The tax rate is 12.5% of actual or assessed annual rental value of the property. The annual value is the amount a property may reasonably gain in rent for one year if the property is offered for lease.

Feel free to contact us if you have any questions: [email protected]

Comments Off on The new inheritance tax regime in Thailand

The Inheritance Tax Act B.E. 2558 (2015) (“ITA”) took effect on 1st of February 2016. It stipulates the following:

1. Inheritance Tax

a. Tax Base

The inheritance tax base shall be calculated from the inheritance, which an inheritor received from each testator, whether it is received once or several times, above 100 Million THB. (Section 12, ITA). The value of the inheritance subject to tax means the value of the asset received as an inheritance offset by the liabilities inherited.

The tax is levied on inheritors who are:

Thai individuals or Thai juristic persons or foreign individuals who are resident in Thailand according to the immigration law, which inheriting assets located in Thailand and outside the country.

Foreign individuals or foreign juristic persons, which inherit assets located in Thailand. (Section 11, ITA)

The spouse of the testator is exempted from inheritance tax. (Section 3(2), ITA)

Foreigners who are resident in Thailand, shall be liable to pay Inheritance Tax in the portion which exceed 100 million THB, calculated from the inherited assets in Thailand and foreign countries. Foreigner who are non-resident in Thailand, shall be liable to pay Inheritance Tax in the portion which exceed 100 million THB, calculated from only inheriting asset in Thailand.

The inheritance tax applies to registered assets, including residential properties, land, vehicles, bonds, equities, and deposits at financial institutions. (Section 14, ITA)

b. Tax Rate

5% of the Tax Base, for inheritors who are descendant or ascendant

10% of the Tax Base, for inheritors who are not descendant or ascendant (Section 16, ITA)

c. Inheritance Tax Declaration

The person liable to pay inheritance tax shall file the “Inheritance Tax Return (Filing)” to within 150 days commencing form the date of receiving the inheritance in total amount of exceeding 100 Million THB. (Section 17, ITA)

2. Penalty

Whoever fail to file a declaration of inherited assets without good reason shall be liable to a fine not exceeding 500,000 THB. (Section 33, ITA)

Whoever destroy, move or transfer any of the inherited assets, shall be liable to imprisonment for not exceeding 2 years and a fine of up to 400,000 THB. (Section 35, ITA)

Whoever file or report a false information or avoid or try to avoid the tax payment shall be liable to imprisonment for not exceeding 1 year or a fine of not exceeding 200,000 THB or both. (Section 37 (1), (2), ITA)

3. Gift Tax

To counter possible avoidance of the new inheritance tax, gift tax was also introduced by way of amending the types of tax-exempt income in the Thai Revenue Code.

For gifts, the tax rate is 5% of the portion above 20 million THB per tax year when the beneficiaries are descendants. For non-descendant beneficiaries, the tax rate is 5% of the portion above 10 million THB per tax year.

Comments Off on Hotel License Application in Thailand – Part 1 of 2

Residential properties which are rented out as daily accommodations for tourists are under intense scrutiny these days in Thailand, in particular with regards to the requirement to obtain a hotel license. The main reason is clearly the high increase of rentals through online portals such as Airbnb.

This is Part I of a blog contribution that discusses the requirements for obtaining such a hotel license under Thai laws and regulations.

Accommodation providers shall apply for a permission from the competent registrar and need to comply with the rules and regulations in order to operate hotel business, if their residential place falls within the definition of hotel in the Hotel Act. The rules and regulations have the purpose of controlling hotel standards, promotion of hotel business operation, promotion and preservation of environmental quality, sturdiness, hygiene and safety of hotels.

Definition of “Hotel”

The definition of “Hotel” under the Hotel Act is stipulated as lodging premises, established for commercial purposes to provide temporary accommodation to a traveler or any person for a consideration (see Hotel Act Section 4). Certain exemptions exist as follows:

any residential premises open to the public for rental with no more than 4 rooms on all floors in total, whether in a single building or in several buildings, and with a total service capacity of not more than 20 guests, operating as a small business which provides an additional source of income for the owners. The owners of such premises are also required to report to the Hotel Registrar;

an accommodation place that is operated by a government authority;

an accommodation place established with an objective to provide accommodation by charging monthly rate only (note that therefore also so-called “serviced apartments” are considered as hotels according to the Act if they provide accommodation on a daily or weekly basis; short term villa rentals, however, are not);

other places that are stipulated in the Ministerial Regulation.

The “Hotel Manager”

Under the Hotel Act, there is a distinction between “hotel operators” and “hotel managers”. The hotel operators are the persons obtaining licenses for hotel operation, while the hotel managers are the persons appointed by the hotel operators who shall be in charge of the hotel management. The hotel operators must notify the registrar of details regarding their hotel managers. The operators can be the same persons as the hotel managers.

The Hotel Act sets forth qualifications which hotel managers (Section 33 Hotel Act) and operators (Hotel Act section 16) must have. Thus the managers for instance must have been awarded a certificate, have experience as prescribed by the Hotel Business Supervision and Promotion Committee (“Committee”) or have a certificate showing that they have attended a hotel management training programs certified by the Committee. The hotel manager can be either Thai or foreign with appropriate visa and work permission.

The Thai Board of Investment (BOI) has introduced its new policy for incentives for qualified investment projects.

Under the new policy, following tax and non-tax incentives may be granted to successful applicants:

Exemption of corporate income tax for up to 15 years

Exemption of import duties:

on machinery

raw or essential materials imported for use in production for export

goods for R&D

Matching grants for:

investment

R&D

Innovation

Human Resources Development

For targeted industries:

Permission to own land for BOI promoted projects

Right to state’s land lease for 50 years and, upon approval, renewal for a further 49 years.

15% personal income tax rate, the lowest rate in ASEAN, for foreign executives working for regional headquarters or international trading companies, treasury centres, along with regional R&D centres.

One stop service center to facilitate foreign investors (Providing useful information, and issuing permits for trading, export and import – all in one location)

Up to five year work visa issuance

These major changes are intended to show strong determination of the royal Thai government in reinforcing the existing foundation and create sustainable business growth with the best mutual benefits for investors, Thailand and all Thai people.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok