Comments Off on First Frank Legal MeetUp – Establishing a Company in Thailand

FRANK Legal & Tax’s first MeetUp on Establishing a Company in Thailand was held successfully on February 10th, 2017 at the company office in Athenee Tower, Bangkok. We plan for the forum to take place once a month, covering a range of subjects related to corporations in Thailand. The next event “Company Formation In Thailand” will take place on March 9th from 18.15-19.45 at our Bangkok office.

Comments Off on FRANK Legal Tax represents fun park company during market entry in Thailand

FRANK Legal & Tax advises and represents a foreign company in legal matters related to establishing fun parks in Bangkok, with a total investment value of approximately 200 Million THB. Our services include the incorporation of a group of companies, license applications and other related matters.

FRANK Legal & Tax is pleased to announce that we have started a “MeetUp” group. The Group aims to to create a forum for entrepreneurs and business start-ups where information can be obtained and ideas can be exchanged.

Comments Off on Multi-Currency Bank Account Can Protect You From Currency Risks

Whether you have business opportunities overseas or are taking care of family members back home, one of the big worries is exchange rates. Even small changes in the dollar’s value can cost you a significant amount, although things could also go in your favor by opening Multi-Currency Account.

Multi-Currency Account or Foreign Currency Account is a bank account that allows for the transfer of payments in different specified currencies to and from one designated account. It can help make your life easier by having the option of multiple currencies in one account, you can easily send and receive money all around the world. If doing business overseas, you want to know what your costs and profits are able to build a reliable plan, not be taking a gamble on the dollar’s future direction.

In Thailand, there are several banks that provide service for Multi-Currency Account. Whether you’re a foreigner or Thai national, you can open a Multi-Currency Account. We explain the details of benefit, type and documents requirement below;

Types of Account:

There are two types of account for Resident Account and Non-Resident Account:

1. Foreign Currency Deposit (FCD) for Resident Account

a. Special Foreign Currency Deposit (SFDC)

If your income comes from overseas and you would like to save it in foreign currency, with an unlimited balance, the Special FCD is suitable for you. It is ideal for traders or anyone with regular earnings in foreign currency without future payment obligation.

b. Domestic Funds – Foreign Currency Deposit (DFCD)

If you have foreign income from international trade or want to save in a foreign currency, you can open a Domestic FCD to manage your export earnings and other foreign income. These accounts are suitable for anyone who wants to save in a foreign currency such as individuals who have international trade businesses. However, this type will require documents showing future foreign currency payment obligations.

c. Domestic Funds – special Foreign Currency Deposit (DSFCD)

Similar as Domestic Funds – Foreign Currency Deposit but without future payment obligation and minimum balance of USD 5 million or equivalent in other currencies.

2. Foreign Currency Deposit (FCD) for Non-Resident Account

Benefit:

One of the major benefits of a foreign currency account is you can send and receive funds in different currencies without exchanging them. This is ideal for anyone in the import and export business to moderate risk exposure from oscillations in exchange rates. For international businesses, it’s also facilitate foreign currency management. You also can easily conversion from one currency to another, to take advantage of any foreign exchange movement.

Please don’t hesitate to contact us if you require assistance with the opening of such an account at a Thai bank, or if you have any questions.

Comments Off on The daily minimum wage in Thailand increases in 2017

Starting from 1 January 2017, the daily minimum wage in Thailand will increase by 1.7% to 3.3% (amount depending on province) in most provinces of Thailand. This increase has been approved by Central Wage Committee on 19 October 2016.

ML Puntrik Smiti, Labour Ministry permanent secretary, stated that eight provinces will maintain a minimum salary of 300 THB, including Trang, Ranong, Sing Buri, Nakhon Si Thammarat, Narathiwat, Pattani, Yala and Chumphon Province. However, the minimum wage in Nonthaburi, Pathum Thani, Samut Prakan, Samut Sakhon, Phuket, Nakhon Pathom and Bangkok will increase by 10 THB (to 310 THB or 8.8 USD per day), by 8 THB (to 308 THB or 8.7 USD per day) in 13 other provinces and by 5 THB (to 305 THB or 8.6 USD per day) in other 49 provinces. The committee will submit its resolution to General Sirichai Distakul, Minister of Labour, then will forward it to the Cabinet.

The increase complies with the regulation of Labour Protection Act by considering 10 factors of Costs of Living, Inflation, Cost of Production, Price of Production, Production Ability, Standard of Living, Product and Service Price, Business Ability, Gross Domestic Product and Economic and Social Conditions.

The Federation of Thai Industries deemed that increases in the minimum wages should vary in each province. The employers are expected to be agreeable to the proposed increases. Anyway, a suitable time schedule needs to be considered as the economic recovery is not yet certain. While the increase may have an impact on small and medium enterprises, employers would be able to adjust to the new figures as there have been no increases in the past three years said Chen Namchaisiri, chairman of the Federation of Thai Industries.

Comments Off on Termination of Employment : Part III – Lay-Off Termination

What are the definitions of “termination” and “lay-off”?

Termination of employment is an employee’s departure from a job. Termination may be voluntary on the employee’s part, or it may be at the hands of the employer, often in the form of dismissal (firing) or a layoff.

Dismissal or firing is generally thought to be the fault of the employee, whereas a layoff is generally done for business reasons (for instance a business slowdown or an economic downturn) outside the employee’s performance.

Checklist:

If you decide to terminate an employee with an unlimited temporary employment, please pay attention our following advice for a correct termination:

1. Notice period

The employer must mind the notice period which ends on the date of the next wage payment. This is usually the last working day of the month following the termination notice.

E.g.: A termination notice is submitted on 10. February. The notice period then ends on 31st March (presumed that the 31st march is not on a weekend or public holiday).

Remark regarding probation period

The requirement for a notice period applies for the first 120 workdays as well.

Therefore, an employee in a probation period must be given the same notice period;

A paragraph in the employment contract which allows the employer to layoff without notice during the probation period is void;

If the employer does not observe the notice period, the employee is entitled to wage payment during the notice period (“wage in lieu of advance notice”)

2. Severance pay

An employer shall pay severance pay to an employee who is laid off. The amount of the severance pay varies, depending on the period of employment:

Remark: the employer is not required to pay severance to an employee whose employment is terminated with cause ( -> Please see our client memo on dismissal of an employee with cause )

Two special cases for severance pay:

a) reorganization measures due usage of machines

In this case, the employer must to make an announcement of an intended termination 60 days in advance and inform the “Labour Inspector”

If the employer neglects the period, he must pay special severance in amount of the wage payment for 60 days beside the regular severance pay (“special severance pay in lieu in advance notice”)

b) relocating of the workplace

If the employee is unwilling to work at the new workplace, he has the right to terminate the employment.

In this case, the employee has the claim to get the full regular severance pay

The Employer shall pay wages of the employee for annual holidays in the year of termination equal to the proportion of annual holidays to which the employee is entitled. Also, Overtime Pay and Holiday Overtime Pay to which the Employee is entitled shall be paid within three days from the date of the Employee’s termination

Comments Off on Termination of Employment : Part II – Dismissal of an employee

What are the definitions of “termination” and “dismissal”?

Termination of employment is an employee’s departure from a job. Termination may be voluntary on the employee’s part, or it may be at the hands of the employer, often in the form of dismissal (firing) or a layoff. Dismissal or firing is generally thought to be the fault of the employee, whereas a layoff is generally done for business reasons (for instance a business slowdown or an economic downturn) outside the employee’s performance.

Dismissal is when the employer chooses to require the employee to leave, generally for a reason which is the fault of the employee. In the case of the dismissal of an employee, the contract ends without notice and without severance pay.

Checklist:

If you decide to dismiss an employee (termination without notice), please pay attention our following advice for a correct termination.

1. Existence of an important reason

Under Thai law, a dismissal is considered under the following circumstances:

being dishonest in performing duties or intentionally committing a criminal against the employer

intentionally causing damages to the employer;

performing an act of negligence which causes severe damages to the employer;

violating work rules or regulations or disobeying the employer’s orders which are legal and fair and which the employer has already given a warning letter, except in serious cases for which the employer is not required to give a warning;

neglecting the work duties for a period of three consecutive work days without a reasonable cause, whether or not there is a holiday intervening in such period; and/or

having been imprisoned by a final judgement.

If one of the aforementioned cases is committed with negligence or is a petty case, the employer must prove that he has suffered a damage.

2. Ultima Ratio (“the last resort”)

The extraordinary termination should always be the last resort. The employer must consider any other measure that may solve the problem like:

transfer to another workplace or department; and/or

ordinary termination.

3. Declaration of the dismissal

The employer should name the important reason in the termination letter. If it is missing, the employer cannot invoke to this reason in a future proceeding.

It is commendable to secure oneself with warning letters (please see our FLT memo related to “Warning Letter to Employee”)

4. Provide the employee with the termination letter

The termination letter should be provided via post or personally.

The employee can have the termination reviewed by the Labor Court. If the Labor Court finds that the termination was unjust, the employer may be ordered to letting the employee work under the old conditions.

If it comes to the result the termination was unjust, but the continuation of work is unacceptable, the employer has to compensate for damages.

5. Practical measures

If the employee leaves the organization, certain things need to be managed, for example:

a) Return of property

If the employee used employer property as a part of the job, make sure you collect them. For example:

company laptop

cellphone

office keys

ID badges

b) Cancellation of any access

You should cancel any access the employee might have to the office. Files, computer files should be protected and make sure that your IT staff cancels passwords to any company digital files. For example:

disconnect the computer login

remove the email address from the staff list

disable entry building code or entry swipe card

For the e-mail-address, make an arrangement with your ID-administrator to determine exactly for how long this account will be active, to avoid unauthorized use by the departing employee.

c) Cancellation of advantages

Make sure that you cancel employee benefits. For example:

Health-, Dental-, Life-, Disability Insurance

Stop retirement contribution

d) Final pay

Make sure that your payroll department calculates the final hours of work as well as any unpaid vacation hours and let the employee know when he or she can get them.

Comments Off on Two Months Deadline For Unlicensed Hotel In Phuket

Unlicensed hotel in Phuket were given a deadline to do the required registrations before 31st January 2017 by Chokchai Dejamornthan, Phuket Governor. If they do not comply, owners may have to confront legal action.

Mr. Chokchai also said that according to Provincial Administration’s information there are only 424 licensed hotels in Phuket while an estimation of 1,366 illegal hotels are currently under operation. The Phuket Provincial Administration gives an opportunity for unlicensed hotels to submit application together with the supporting documents at district office within 2 months. After expiration of this deadline, such hotels will be closed by Phuket Provincial Administration.

During a public meeting with government officials it was announced that the crackdown would be starting from 1st December 2016. The main targets are residential properties such as apartments or condominiums who rent out daily accommodations for tourists and the main reason is due to the high increase of rentals through AirBnB.

On 7th of June 2016, the new Land and Building Tax Act (the “Act”) was formally enacted. The Act will likely become effective in early 2019 and will be replace the existing and old Land and House Tax Act B.E. 2475 (1932) and the Local Development Tax B.E. 2508 (1965).

The new law will introduce an entirely new system of property taxation. While the previous system focused on gains derived from property, going forward an annual tax payment for the property as such will be implemented. This will likely increase the tax burden for owners of larger land areas and for land banking.

Under the Act, tax payer is the

1) Owner of land and structures;

2) Owner of condominium; and

3) Possessor or beneficiary of land or structures on government property.

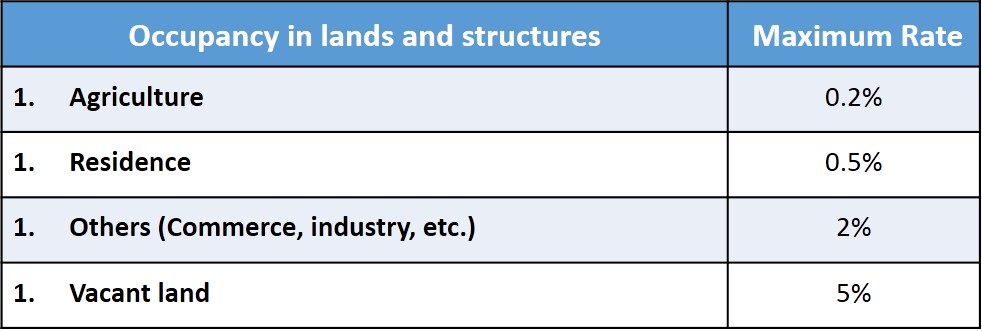

The maximum tax rates vary, depending on the type of occupancy of land and structures:

Above rate represents the maximum rates under the Act, the actual tax rate will be set forth by royal decree.

Please see more detailed stipulations of the tax rates as follows:

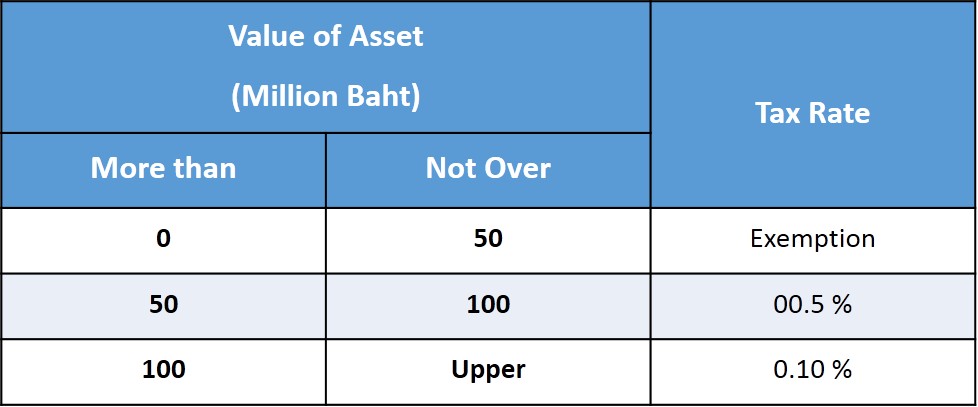

1. Lands and structures for agriculture and the first residence

2. Land and structures for other residence

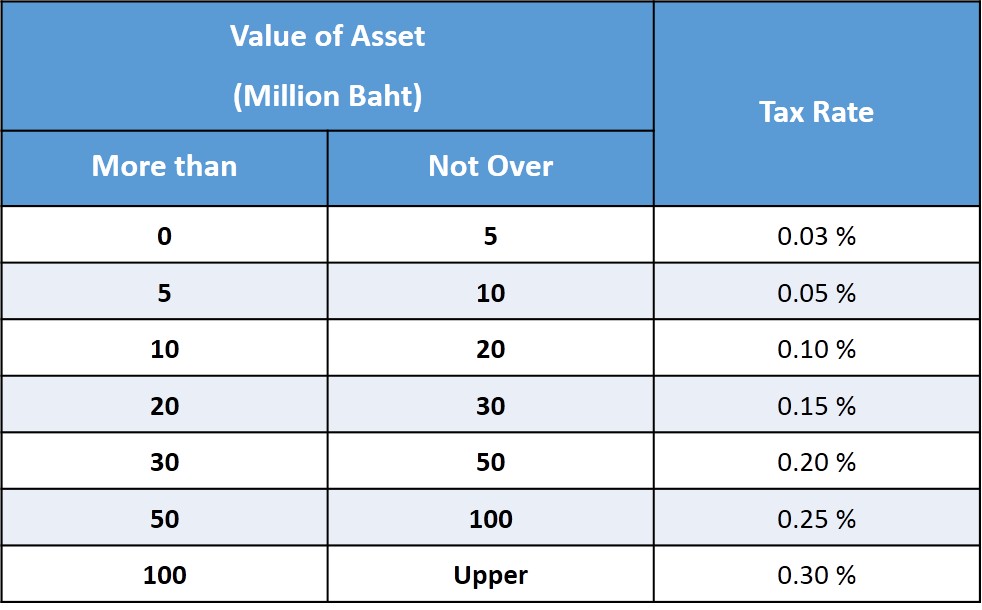

3. Land and structures for other use (Commerce, industry, etc.)

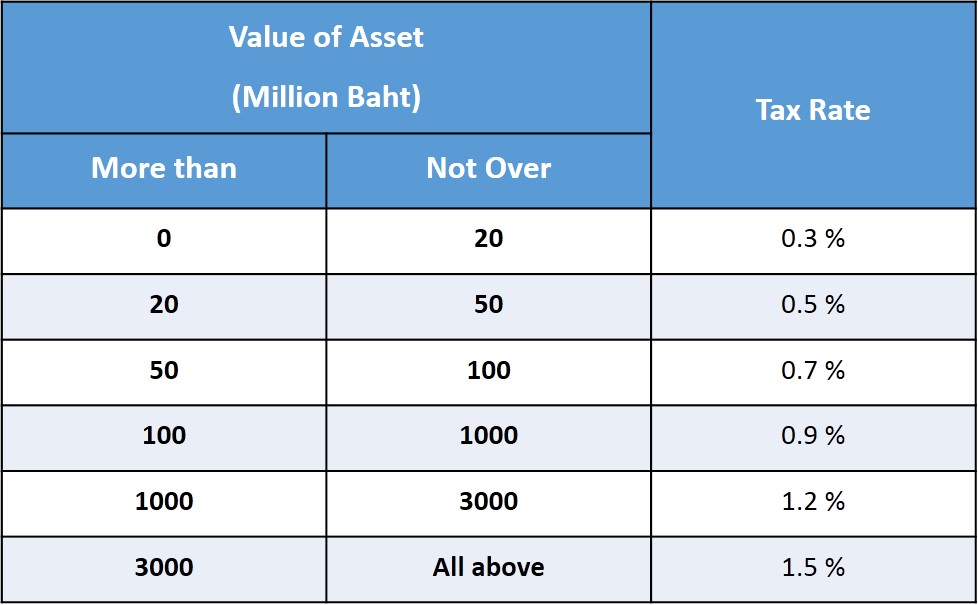

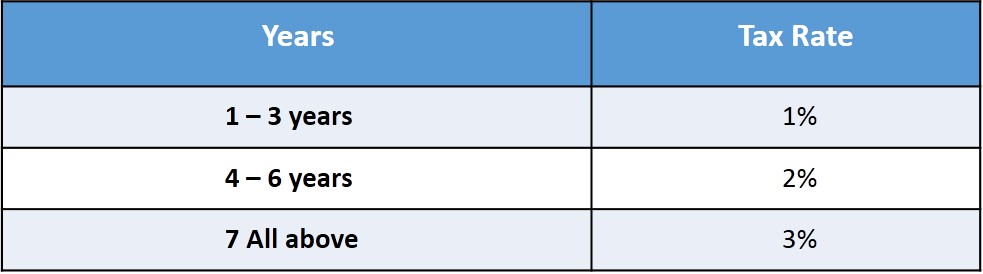

4. Vacant land

Tax rate will increase every 3 years for support land owner develop their land.

Again, the above rates represent the maximum rates under the Act, the actual tax rates will be set forth specifically.

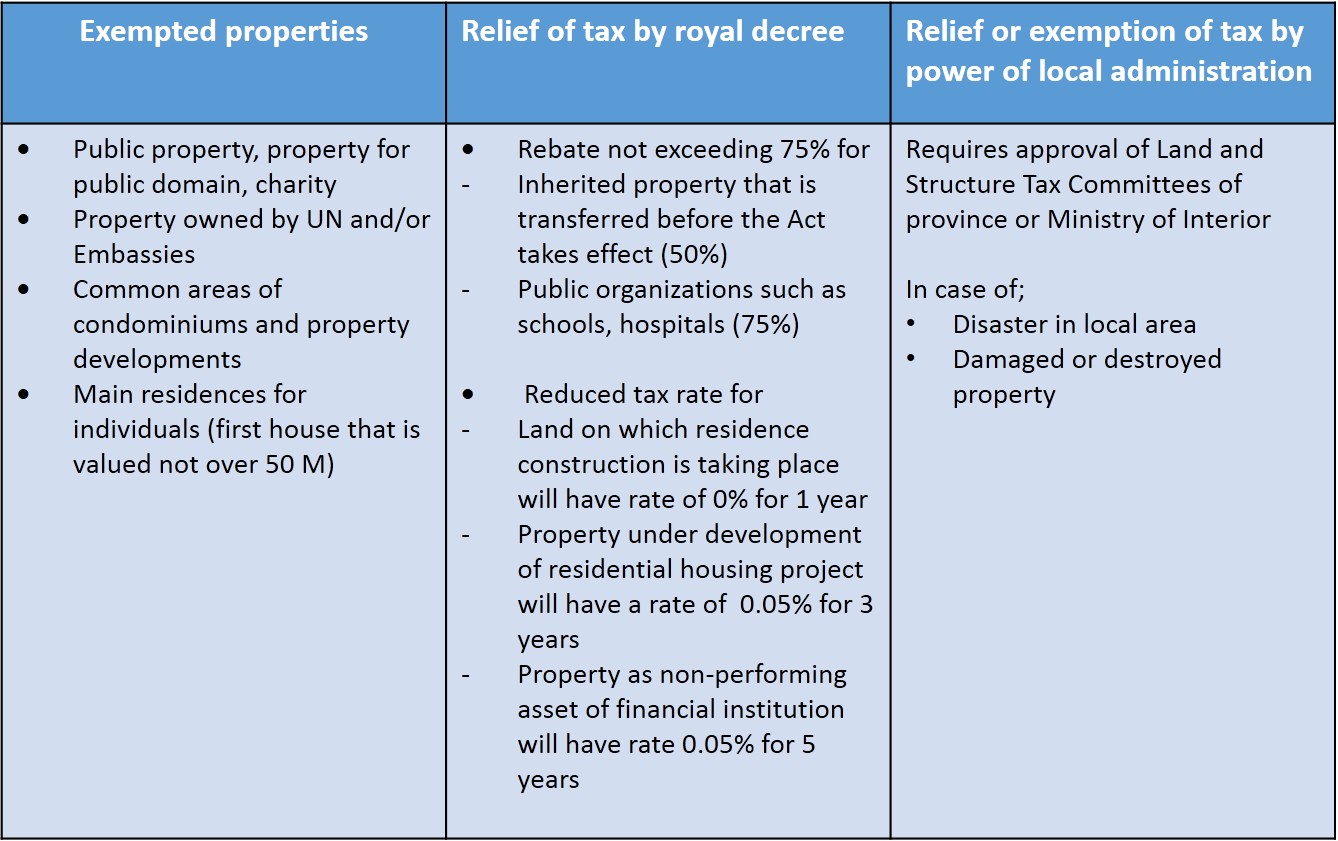

5. Tax holiday

Following properties are exempted or relieved from the new tax:

The tax burden will be calculated on the basis of the value of land and structure (according to the Land Department index values):

Tax Burden = (Value of land + Value of structure) * Tax Rate

Value of Land = Estimated value of Land * Area

Value of Structure = [Estimated value of structure * Area] – Depreciated Value

Please feel free to contact us if you have any inquiries regarding the above: [email protected]

It should be noted that a restaurant business often entails the requirement of other licenses, such as a liquor license. Before a restaurant, store or bar can serve liquor in Thailand, it must obtain a liquor license from the Excise Department under Section 17 of Liquor Act B.E. 2493 (1950). A liquor license is a permit that allows an establishment to legally sell alcohol. Establishments that require liquor licenses include pubs, bars, restaurants, distillers, importers, distributors, wholesalers, hotels, clubs, theaters, grocery stores and liquor stores. To obtain the liquor license, the applicant must contact and file the application with the District Office or Local Excise Department. The penalty for any violation of this act would be a fine.

General requirements for liquor license are:-

Copy of company affidavit,

Copy of lease agreement of business establishment and consent letter from the landlord,

Copy of house registration of business establishment, and

Map of liquor establishment for distribution,

The liquor license is valid for one a year. The license must be annually renewed before its expiration.

After the liquor license has been acquired, the licensee may sell the liquor in the specific place, date and time prescribed by the official. The liquor must not be transformed by contaminating with any other ingredient or type of liquor thereto without the official permission.

Under the Alcohol Beverage Control Act, B.E. 2551 (2008), it is prohibited to sell liquor in close proximity to schools, religious areas and gas station. It is also forbidden to provide any sale promotion to the liquor. Otherwise, a penalty of imprisonment and fine may be imposed.